1

Q2 Earnings Review

July 26, 2011

Exhibit 99.2 |

| 1

Q2 Earnings Review

July 26, 2011

Exhibit 99.2 |

2

Cautionary Notice: Forward-Looking Statements

This

presentation

contains

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities Litigation Reform Act of 1995. These statements relate

to future events, are not historical facts and are based on our

current expectations and assumptions regarding our business, the economy

and other future conditions. These statements can generally be

identified by lead-in words such as

“believe”,

“expect”,

“anticipate”,

“intend”,

“plan”,

“foresee”,

“may”,

”will”

and

other

similar

words.

Statements that describe our Company’s objectives, plans or goals

are also forward-looking statements. Examples of such

forward-looking information we may be discussing in this presentation

include, without limitation, further implementation of our operational

strategies and playbooks, future debt retirement, capital

expenditures, operating margins and revenues, inventory levels and new

vehicle industry sales volume.

You are cautioned that these forward-looking statements are not

guarantees of future performance, involve risks and

uncertainties and actual results may differ materially from those projected in the

forward-looking statements as a result of various factors.

These risks and uncertainties include, among other things, (a)

economic conditions in the markets in which we operate, (b) the success of

our operational strategies, (c) our relationships with the automobile

manufacturers and (d) new and used vehicle sales volume. These

risks and uncertainties, as well as additional factors that could affect

our forward-looking statements, are described in our Form 10-K

for the year ending December 31, 2010 and our Form 10-Q for

period ended March 31, 2011. These forward-looking

statements, risks, uncertainties and additional factors speak only as of the

date

of

this

presentation.

We

undertake

no

obligation

to

update

any

such

statements. |

3

Sonic Automotive Q2 2011

o

Quarter in Review

o

Financial Results

o

Operations Recap

o

Summary and Outlook |

4

Overall Results

Grow the base business

Revenues up 14%

New vehicle revenue up 16.0%; Volume exceeds industry growth

Used revenue up 15%

F&I revenue up 22%

Fixed Operations up 6.0%

SG&A to Gross declined to 77.6%

Income from continuing operations up 59.1% *

Q2 2011 diluted EPS from continuing operations was $0.37 per share, an

increase of 54.2% from Q2 2010 *

Completed extension of floor plan and revolving credit facilities

* Calculated excluding the $7.3M debt

extinguishment charge recorded in Q2 2010 |

(dollars in millions, except per share)

B / (W) than Q2 2010

Q2 2011

$

%

Revenue

1,968

$

246

$

14%

Gross Profit

310

27

10%

Operating Profit

59

11

23%

Non-Floor Plan Interest

18

2

10%

Continuing Operations

-Profit After Tax

22

$

13

$

(1)

131%

-Diluted EPS

0.37

$

0.19

$

(1)

106%

Discops EPS

(0.02)

$

-

$

Memo: SGA % of Gross

77.6%

230

bps

Second Quarter Results

(1)

Prior year includes an after-tax charge of $4.3 million, or $0.06

per diluted share, from loss on debt repurchases.

5 |

(dollars in millions)

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Revenue

1,544

$

1,722

$

1,770

$

1,845

$

1,839

$

1,968

$

Gross Profit

266

282

282

285

291

310

SG&A Expense

221

$

226

$

226

$

224

$

233

$

240

$

SG&A as % of Gross Profit

83.0%

79.9%

80.3%

78.8%

79.9%

77.6%

SG&A

Leveraging

SG&A Expenses

6 |

Capital Spending

7

Actual

1st Half

2011

Expected

2nd Half

2011

Expected

FY 2011

Facility Improvement

26.6

$

7.0

$

33.6

$

Real Estate Acquisitions

75.2

5.0

80.2

Less: Mortgage Funding

(54.0)

(15.0)

(69.0)

Net Cash Used - Facility Related

47.8

$

(3.0)

$

44.8

$

IT Capital Spending

3.9

5.8

9.7

Maintenance Cap Ex

7.0

3.0

10.0

Total Cash Used - Cap Ex

58.7

$

5.8

$

64.5

$

(amounts in millions) |

Credit Facility

•

Extended term:

August 15, 2016 maturity (was August 2012)

•

Increased size:

Revolving Credit Facility -

$175.0 million ($25.0 million increase)

New Vehicle Floorplan Facility -

$500.0 million ($179.0 million increase)

Used Vehicle Floorplan Facility -

$80.0 million ($30.0 million increase)

•

Improved flexibility to focus on our strategic priorities of

reducing non-mortgage debt and owning our property

8

Note:

On

July

15,

2011,

we

issued

a

redemption

notice

to

holders

of

our

8.625%

Notes

to

redeem

$42.9M in aggregate principal of the 8.625% Notes on August 16,

2011. |

New Retail Vehicles

Q2

Q2

(dollars in thousands, except GPU)

2011

2010

B / (W)

New Retail Volume

28,367

(1)

24,647

15.1%

New Gross Margin

6.8%

6.9%

(10)

bps

New GPU

2,351

$

2,364

$

(0.6%)

New Gross Profit

66,680

$

58,273

$

F&I Gross Profit - New

34,774

$

27,913

$

Industry SAAR (millions)

12.1

11.3

7.1%

9

Up 18%

Overall:

Expect

J3

inventory

allocations

to

improve

as

summer

progresses.

Incentives:

Expect J3 incentives to increase as production resumes.

Domestics:

Wait and see attitude toward incentives and market share.

Demand:

Expect SAAR levels to return to pre-disaster levels in late

Q3. (1) Sonic new retail volume was 0.9% of U.S. auto unit

sales – Source: Bloomberg Financial Markets |

10

Used Retail Vehicles

Q2

Q2

(dollars in thousands, except GPU)

2011

2010

B / (W) %

Used Retail Volume

27,141

24,382

11.3%

CPO Volume

7,843

8,342

(6.0%)

Used GPU

1,458

$

1,542

$

(5.4%)

Used Gross Profit

39,560

$

37,586

$

5.3%

Used to New Ratio

0.96

0.99

F&I Gross Profit - Used

21,007

$

17,701

$

18.7%

Total Fixed Ops

147,785

$

141,804

$

4.2%

All-

Time

Record |

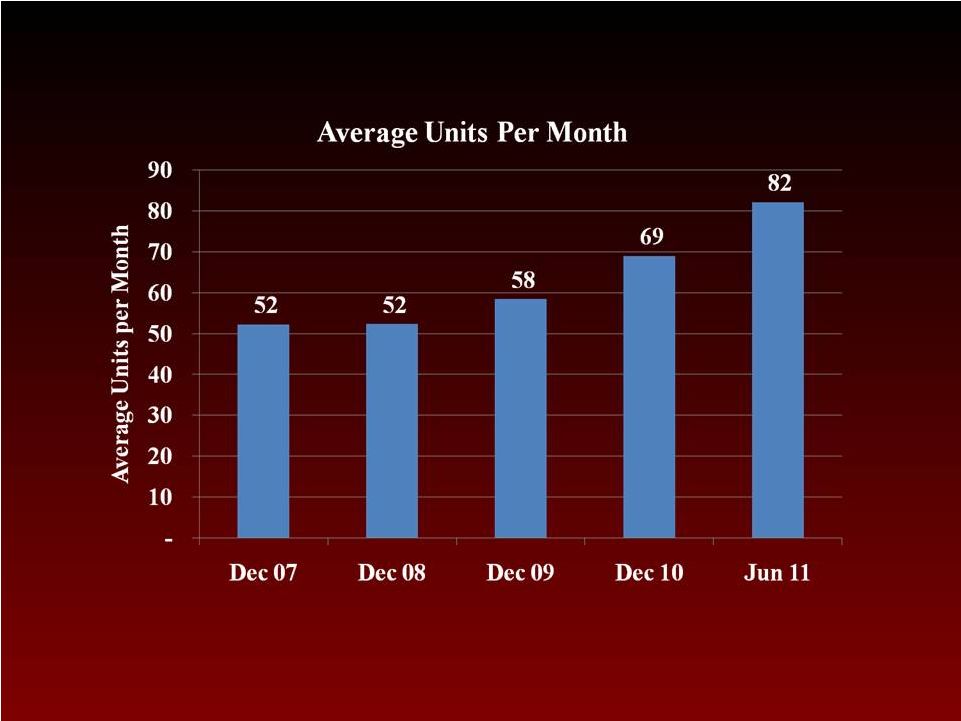

Used Volume –

Tracking 100 per Store

# Stores Averaging 100+ per Month:

9

7

17

21 25

11 |

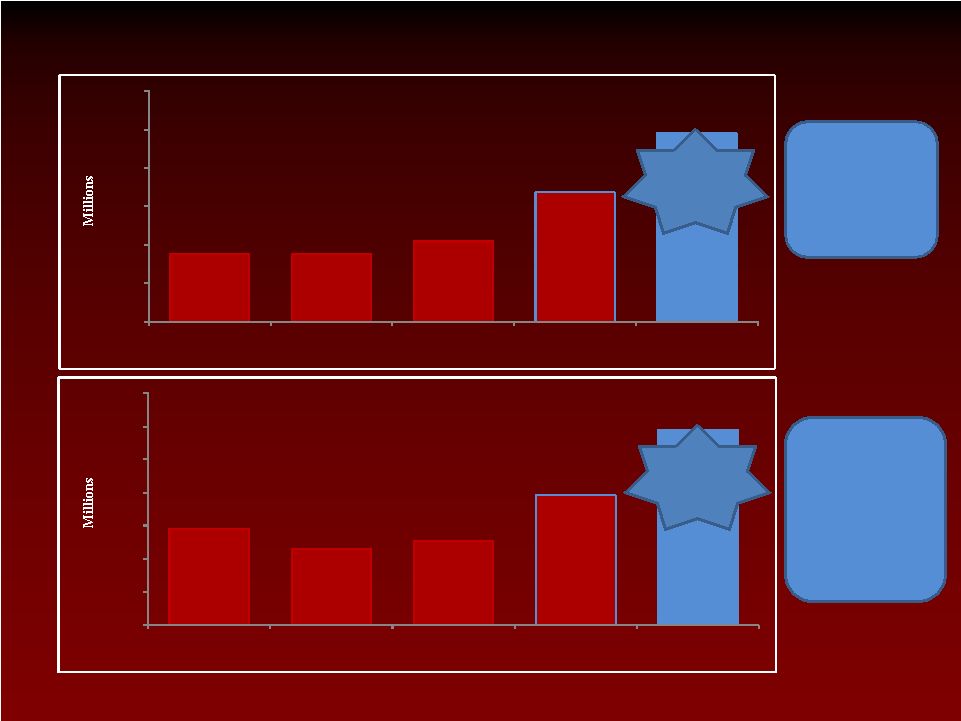

Fixed Operations

YOY Sales

Increase of

$15.7M, or

5.5%

Gross

Margin was

49.3% and

Fixed Abs

was 88% in

Q2 2011

12

$141.8

$140.6

$141.1

$143.9

$147.8

$136

$138

$140

$142

$144

$146

$148

$150

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Gross

$283.8

$283.7

$285.4

$291.8

$299.5

$275

$280

$285

$290

$295

$300

$305

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Sales

All-

Time

Record

All-

Time

Record |

13

Summary

Base business continues to grow

New vehicle market share continues to increase

Used retail vehicle volume continues to grow at double-digit

rate

F&I benefiting from growth in new and used volume

Leveraging SG&A as gross profit grows

Automotive retail industry continues its steady recovery

Still forecasting a 12.5 million SAAR

Expect Japanese brands to improve in 2H of Q3

Maintain

continuing

operations

earnings

guidance

of

$1.18

-

$1.28

for FY 2011 |